Remote solar design tools have made the sales process faster and cheaper. A rep can build a proposal, generate a shading analysis, and submit it for financing without ever visiting the site. That convenience is real, but it comes with a significant downside.

Remote 3D design environments are adjustable. The same flexibility that lets a designer refine a layout to fit a roof also allows someone to nudge variables in ways that improve a project’s numbers on paper without improving the actual system. Finance companies reviewing these submissions often lack the tools or technical depth to detect the changes.

The consequences hit homeowners first and finance company portfolios second. According to Scanifly’s internal survey data, over 25% of projects face revisions or redesigns on install day. One TPO QA team leader who reviews hundreds of submissions daily, noted that roughly 40% of projects face rejection due to shading analysis issues. A separate TPO reported 5% to 30% deltas between actual and forecasted production across their portfolio. One large TPO fund is paying in no sooner than several weeks, in part because of having to understand the designs.

Here’s exactly what’s happening, and what to do about it.

The Four Ways Remote Designs Get Manipulated

1. Adjusting LiDAR height offsets

Most solar design software allows sales reps or designers to offset LiDAR data along the Z-axis to align the model with satellite imagery. This is a legitimate calibration function.

However, adjusting that offset by even 10 to 15 feet meaningfully reduces the shade impact of surrounding obstructions. A neighboring structure that would cast significant shade at its correct height casts much less at an artificially lowered one.

There’s no disclosure requirement, no flag in the submission, and no easy way to detect it without independent site data.

2. Manipulating tree heights and widths

Solar contractors and reps can easily adjust tree heights in a remote design by five to ten feet, and a QA reviewer has no way to detect it. Depending on the site, that small change can significantly shift shading percentages and production estimates. Or it can make just enough of a difference to pad a rep’s commission without anyone noticing either way.

Why does this matter so much? Trees are typically the primary shading factor on residential projects, particularly in high-vegetation markets. LiDAR data captures tree canopy geometry at the time of the aerial survey, which may be years out of date.

Most design tools render trees as simplified geometric shapes that don’t reflect actual canopy structure, meaning reps can shrink heights, reduce canopy widths, or reposition them entirely without raising any flags. Finance companies reviewing the shade report have no reference for what those trees actually look like today without onsite data.

3. Switching shade data layers without disclosure

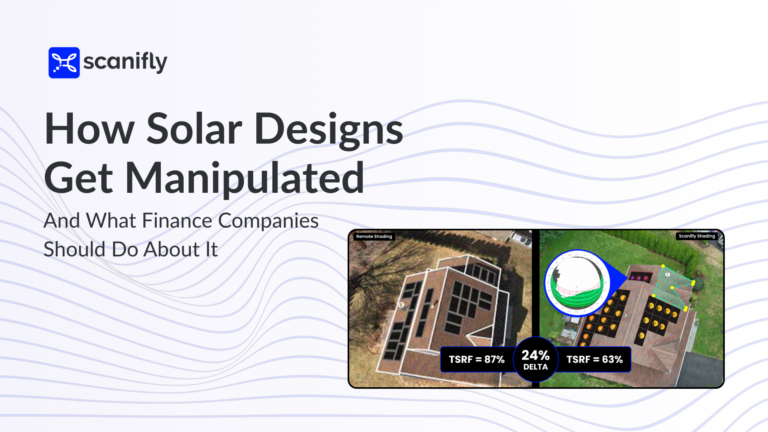

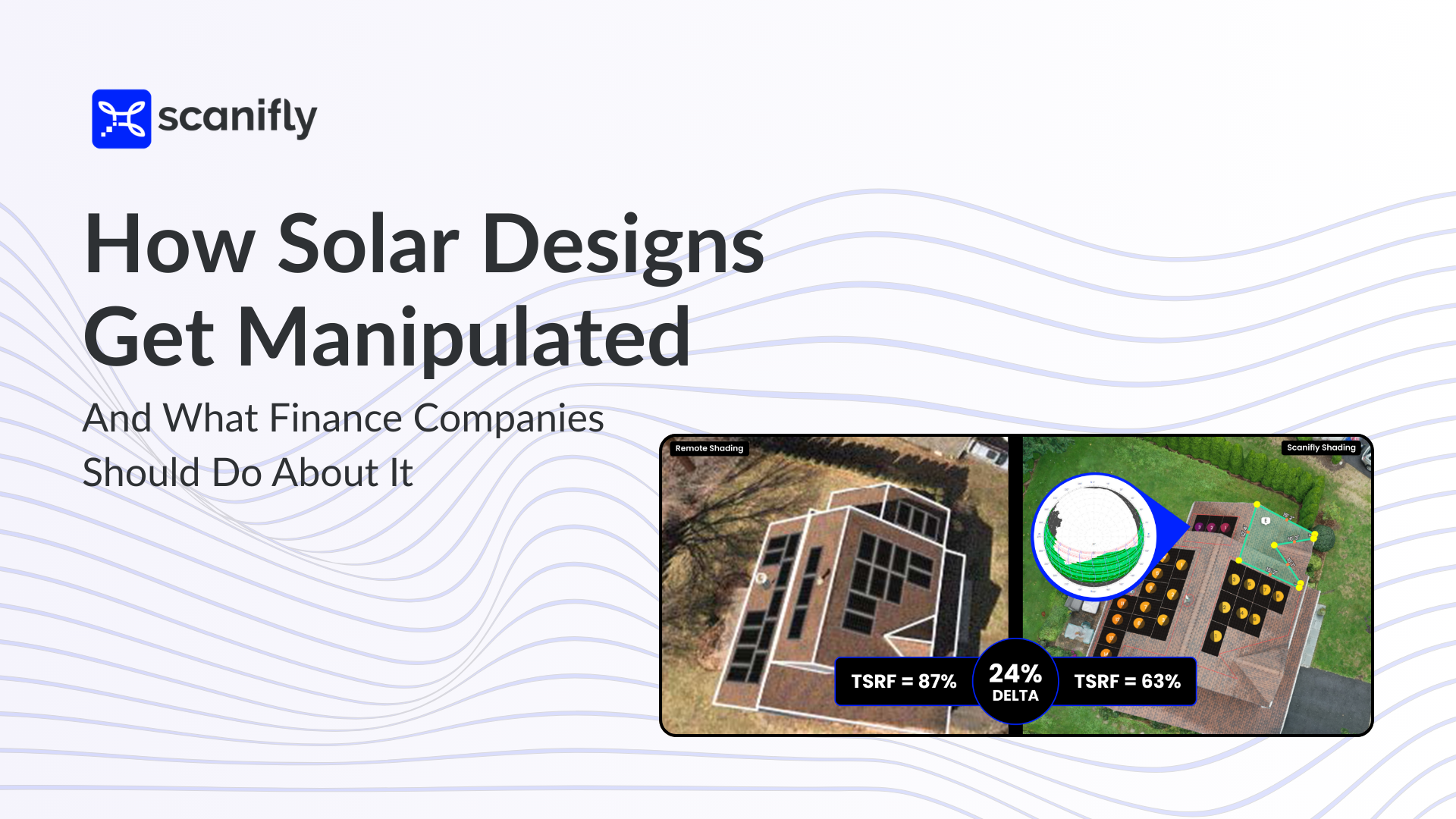

Most design tools now offer multiple shade data sources: LiDAR, Google 3D, satellite imagery, and others. Switching between them is surprisingly easy, and reps rarely disclose which one they used in the final submission. Unfortunately, an unethical rep can simply shop for whichever layer produces the most favorable production estimate.

A common example: LiDAR data shows significant tree coverage on a property, but the Google 3D layer doesn’t capture those same trees. A rep who knows this can submit the Google 3D layer, pass QA review, and walk away with a higher commission. Most finance companies review the submission at face value without cross-referencing multiple shade sources. And even when a reviewer catches a discrepancy, the industry still hasn’t answered a more fundamental question: which shade data is actually the source of truth?

Without disclosure requirements, a reviewer has no way of knowing which source the rep used, how old the underlying data is, or whether the rep changed the layer at any point during the design process.

4. Tweaking module spacing to fit more panels

Racking systems have specific module spacing requirements, and fire setback rules vary by jurisdiction. Reducing module spacing in a design, or interpreting fire setbacks more aggressively than local code allows, allows a sales rep to fit more panels into a given roof section.

More panels mean a larger system and a higher production estimate. It also means a system that may not actually fit the roof as designed. By the time that problem surfaces on install day, the finance company has already approved the deal based on an inflated layout.

What Finance Companies Should Do About It

None of these problems require expensive solutions. They require finance companies to upgrade disclosure requirements and submission standards. There are few finance companies in the post-25D world, and they have the leverage to enact changes.

Require disclosure of the shade layer in every submission.

Every project submission should state which shade data source the rep used, the age of that data, and whether the designer made any manual adjustments to LiDAR offsets or obstruction geometry. A rep who knows the finance company will scrutinize those modifications is less likely to exploit them.

Flag and investigate edited LiDAR submissions.

When a designer has adjusted LiDAR offsets beyond a reasonable range, that should be a required disclosure and a trigger for additional review.

Finance companies can establish threshold rules: adjustments within a reasonable tolerance are acceptable with disclosure, while adjustments beyond that threshold require independent verification or an onsite survey.

Request a drone-based 3D model for high-value projects.

Drone-based photogrammetric models reflect current, site-specific conditions that remote data cannot match.

For projects above a certain system size, in markets with known data quality issues, or from contractors with histories of high revision rates, requiring a drone model as part of the submission is a practical and proportionate ask.

Scanifly’s DroneDesign produces inch-accurate 3D models of the actual roof and surrounding environment, as well as real-time onsite shading analysis, so the system performs exactly as quoted and installs exactly as designed.

Incentivize onsite data collection.

Finance companies and TPO providers can offer preferential treatment, faster review timelines, wider production tolerance bands, and streamlined approval for projects that include verified onsite data. Austin Energy already requires it. The Energy Trust of Oregon incentivizes it.

As Scanifly outlined in its piece on TPO financing standards, TPO providers have the leverage to make this shift right now. The same logic can apply to loan and lease providers.

Standardize module spacing and fire setback requirements.

Define acceptable racking spacing and jurisdiction-specific fire setback assumptions as part of submission requirements. Designs that fall outside those standards should trigger review. This is basic underwriting hygiene that most finance companies haven’t formalized.

The Bottom Line

Solar has historically operated like the wild west in many markets, with reps and contractors learning to exploit the flexibility of remote design tools to their advantage. To their credit, finance companies and regulators have begun to adapt, and many reps are genuinely leveling up their quality and ethics. Overall, the industry is slowly cleaning itself up.

That said, finance companies still have more work to do. As capital providers, they control what they finance and what standards reps must meet to access that capital. Reps will always maximize their returns within the rules set by finance companies. That’s rational behavior. What’s less rational is ignoring how design-quality problems quietly accumulate within a portfolio over time. The finance companies that looked the other way on quality long enough are largely no longer around, and poor fund performance had a lot to do with it.

Today, a small number of TPO providers control the majority of the market—LightReach, GoodLeap, IGS, and a handful of others—alongside a growing wave of smaller prepaid companies. That concentration of capital is a real opportunity. Demanding disclosure of the shade layer is a reasonable starting point, but that alone won’t eliminate manipulation. The real win is incentivizing verified, real-time onsite data. Contractors who have made that shift will tell you it doesn’t just improve operations. It has proven to help close more sales too. Finance companies have the leverage to make it the standard, and now is the right time to use it.

Frequently Asked Questions

How can solar designs be manipulated without detection?

Remote solar design environments allow adjustments to LiDAR height offsets, tree geometry, shade layer selection, and module spacing, all of which affect production estimates. Without disclosure requirements or independent site verification, finance companies have no reliable way to identify when these adjustments have pushed estimates beyond what the real site will support.

What is a shade layer in solar design and why does it matter?

A shade layer is the data source used to model the 3D environment around a solar installation, including trees, neighboring structures, and other obstructions. Different shade layers vary in age, point density, and coverage, and the choice of layer directly affects production estimates. Most project submissions don’t disclose which layer was used or how old the data is.

What should finance companies require in a solar project submission?

At minimum: disclosure of the shade data source and its vintage, disclosure of any manual adjustments made to the design, compliance with standardized module spacing and fire setback assumptions, and for higher-value or flagged projects, a drone-based site model or independent site verification.

What is TPO solar financing and how does it relate to design quality?

TPO (third-party ownership) refers to lease and PPA financing structures where the finance company owns the solar system and sells power or leases the equipment to the homeowner. Because TPO providers own the asset over a 20 to 25 year period, design accuracy directly impacts their financial returns. Inaccurate production estimates at point of sale translate directly into underperforming assets in their portfolio.